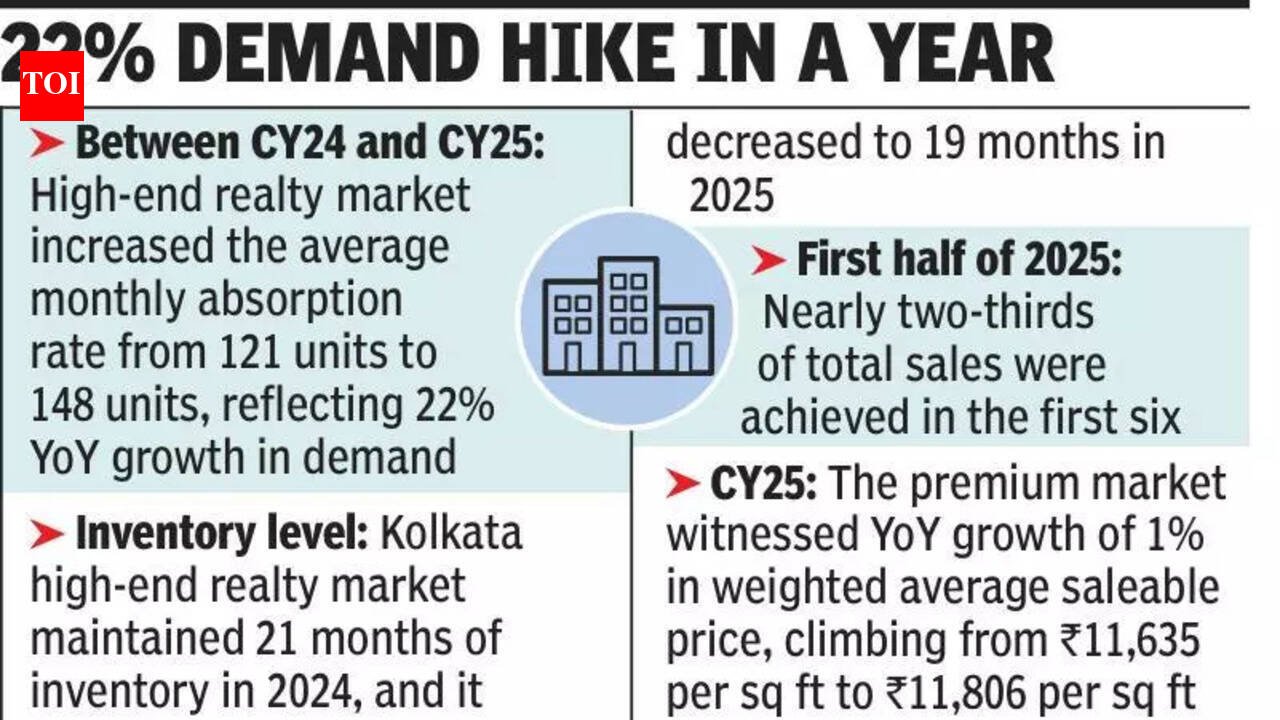

Sales was strong despite higher supply. In CY24, 1,355 units were sold (36% of supply). In CY25, 1,666 units were sold (39% of supply). This translated into 23% YoY growth in sales against 14% YoY growth in supply, indicating demand is outpacing new additions. Unsold inventory also rose (10% YoY), but the market’s ability to convert a larger share of supply into sales showed improving liquidity rather than stress. Monthly average absorption moved up from 121 units in CY24 to 148 units in CY25, and the market saw a sharp front-loading of demand, with 65% of CY25 sales occurring in H1’25—buyers are acting earlier in the cycle, especially on credible launches and scarce micro-markets.Premium pricing stayed firm with a mild upward movement. Weighted average saleable price increased 1% YoY from Rs 11,635 PSF in CY24 to Rs 11,806 PSF in CY25. The key takeaway is price resilience: even with a 14% jump in supply, prices did not soften, suggesting end-user depth and brand-led pricing power. Growth is being driven more by product positioning, location scarcity, and developer credibility than by broad-based market inflation. The market is expanding in breadth (more projects, more units) and improving in speed (higher absorption, higher sales share), while maintaining pricing discipline (only 1% YoY rise in weighted average PSF). South Kolkata remains the volume anchor for premium supply, but New Town and the Bypass–Ruby corridor are increasingly. The strongest momentum is concentrated in branded, well-located, scarcity-backed projects, especially in the first half of the year. The highest sales that happened in CY25 in the segment were 3BHK units. While the count of 3BHK and 4BHK units sold was identical in CY24 at 607, it was 866 3BHK units in CY25 against 685 4BHK units that year. “Rising disposable income and evolving aspirations also drove homebuyers towards premium residences. The share of homes priced above Rs 1.5 crore in Kolkata’s sales basket has grown faster than in most other metros,” said Credai West Bengal president Sushil Mohta.